Kwarkot

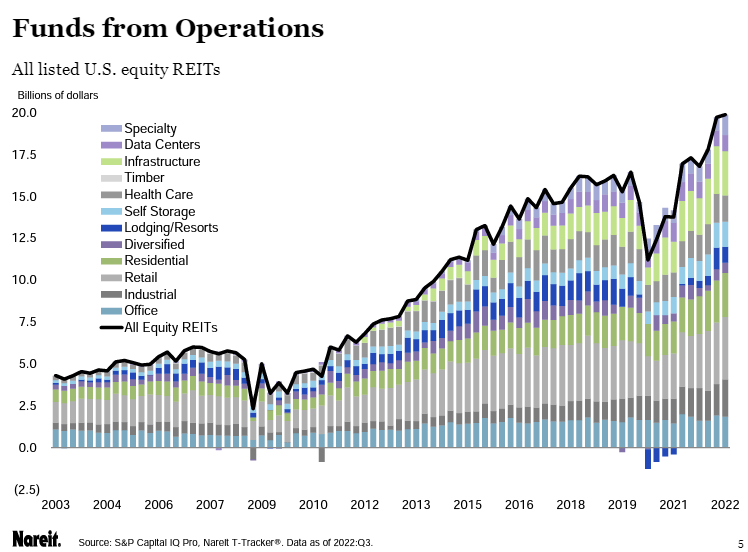

U.S. real estate investment trusts’ (REITs) funds from operations climbed almost 15% to a record $19.9B in Q3 2022 from a year ago, according to the National Association of Real Estate Investment Trusts’ (NAREIT) Q3 T-Tracker. The 14.9% Y/Y increase slowed from 16.4% in Q2 and 29.3% growth in Q1 2022.

A majority of REITs, 81%, reported Y/Y increases in FFO during the quarter. For all listed U.S. equity REITs, net operating income increased 8.1% Y/Y, down from 10.5% in Q2 and 15.2% in Q1.

The quarterly results show a “a degree of normalization,” said John D. Worth, NAREIT executive vice president, Research & Investor Outreach. “We’re seeing some leveling out of the large declines in earnings [when COVID restrictions took hold] followed by very, very large percentage increases as we got into the recovery mode.”

Only three equity REIT sectors haven’t yet overtaken their pre-pandemic levels of FFO — lodging and resorts, data centers, and health care, the last of which is almost back to pre-COVID levels, Worth said.

Lodging & resort REITs are catching up, with the sector logging the strongest FFO percentage growth in Q3, up 126% Y/Y. The next-strongest sector was freestanding retail, up 49.9%, followed by industrial REITs, up 30.9%. Industrial REITs proved to be one of the sectors that benefited the most from the pandemic-era acceleration of e-commerce, as people were largely prevented from traveling for much of 2020.

Overall, dividends paid by U.S. REITs are staying healthy, rising 20.6% Y/Y in Q3, up from 14.6% Y/Y growth in Q2. Mortgage REITs, though saw the Y/Y growth rate slow to 12.2% in Q3 from 19.0% in Q2 and 16.7% in Q1.

With the economic outlook uncertain, and interest rates remaining high, REITs appear to be well prepared. Leverage was near historic lows, with debt-to-market assets at 34.5%. in another encouraging sign, fixed-rate debt accounted for 82.6% of total debt. Interest coverage increased to 6x, and net interest expense, as a percent of NOI, was near its historic low at 18.9%.

In addition, the weighted average term to maturity of REIT debt was 84 months, or more than seven years, which means their debt repayment is spread out over a number of years.

At NAREIT’s recent REITWorld conference, managements are still optimistic about their operating performance, Worth said, but they appear to be more cautious about the 12 months ahead. “We’re still not seeing a lot of our member REITs saying they’re seeing slower growth today in operating metrics, but certainly it’s getting factored into their outlook for 2023.”

One big question mark going forward is when acquisition activity will recover. “A lot of what we’re hearing is transactions aren’t happening because buyers and sellers essentially can’t get on the same page about what the appropriate cap rate for those transactions should be,” Worth said.

That resumption will “undoubtedly is going to come at some point,” he said, but whether it’s in Q4 2022 or next year is yet to be seen.

Even with the higher risk of a recession, publicly traded real estate investment trusts may be better positioned to weather the downturn than the private real estate sector, said Edward Pierzak, NAREIT’s senior vice president of Research.

In the last six recessions, REITs, on average, underperformed private real estate in the four quarters before a recession, but outperformed private real estate during and in the four quarters after a recession.

“We all know that economic growth is really a driver of real estate performance, but that said, even when we look at what would be kind of low real GDP environments, that does not necessarily translate into negative, real estate performance,” Pierzak said.

For a look at the real estate and REIT stocks that rank the best in the SA stock screener, click here.

SA contributor Colorado Wealth Management Fund takes a look at whether apartment REITs can handle higher interest expense

Image and article originally from seekingalpha.com. Read the original article here.